Comparing BDC Interest Rate Sensitivity: August 2022

Rising Interest Rates

Over the last five months, Secured Overnight Financing Rate (“SOFR”) which is the preferred replacement for LIBOR has increased by over 220 basis points which is important because most BDC have floating-rate investments with floors between 25 to 100 basis points (reached earlier this year for most investments). However, depending on the timing of resets (typically quarterly) most BDCs did not have a material impact on earnings for Q2 2022 (discussed below).

Also, most BDCs with variable rate borrowings were negatively impacted during Q2 2022 without the benefit from higher rates in investments. This implies that Q1 and Q2 earnings will probably be the worst quarters for most BDCs followed by healthy increases starting in Q3 2022 which is likely why many BDCs recently increased their regular dividends including PNNT, TSLX, ARCC, MAIN, HTGC, CSWC, OCSL, FSK, MFIC, and CGBD.

TSLX Call: “We expect to see meaningful positive asset sensitivity in the back half of the year. The combination of the rising rates in Q2 are now well above our average floor levels on our debt investments and the shape of the forward LIBOR or SOFR curve support that expectation. The rising rates will drive incremental interest income and outweigh the increases in the cost of our liabilities. To date, this has been largely muted because applicable reference rate resets occurred during -- occurred earlier in the quarter. Based on the shape of the forward curve and reset dates of our issuers, we project the remainder of this year that rate movement loan will result in approximately $0.13 per share of incremental net investment income purely from the core earnings power of the portfolio relative to what we experienced in Q2.”

ARCC Call: “Based on our estimates of increasing earnings from higher interest rates coupled with the strength of our investment portfolio, we have increased our regular quarterly dividend to $0.43 per share. The second quarter increases in market rates have yet to fully flow through our earnings. We estimate our second quarter earnings would have been approximately $0.05 per share higher if the market rate increases during the second quarter would have been in place for the full quarter. We believe we are well positioned for our earnings to benefit from further increases in short term market interest rates.”

HTGC Call: “For the third quarter, we're increasing our core yield guidance range to 11.5% to 12%. As a reminder, approximately 95% of our debt portfolio is floating with a floor. So the recent interest rate hike and any additional in 2022 will benefit our core yield going forward. But the other part of that is also that we're onboarding deals at a slightly higher yield relative to where we were 1 or 2 quarters ago.”

As shown in a table near the end of this update, using historical coverage and the upcoming impacts from previous increases in interest rates there are many BDCs that will likely be the next round dividend increases. It should be noted that most of the BDCs are already considered ‘Level 1’ dividend coverage BDCs.

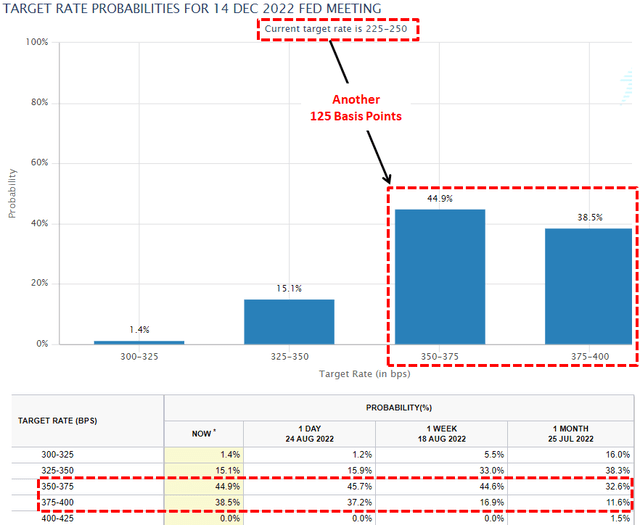

There is currently an 83% chance of the fed funds' lower target rate increasing another 125 basis points or higher over the next 3 meetings (less than 4 months from now).

BDC Interest Rate Sensitivity

Interest rate sensitivity refers to the change in earnings that may result from changes in interest rates. Most companies report interest rate risk/opportunity in the ‘Quantitative and Qualitative Disclosures About Market Risk’ section of the regulatory filings:

“Interest rate sensitivity refers to the change in our earnings that may result from changes in the level of interest rates. Because we fund a portion of our investments with borrowings, our net investment income is affected by the difference between the rate at which we invest and the rate at which we borrow. As a result, there can be no assurance that a significant change in market interest rates will not have a material adverse effect on our net investment income.

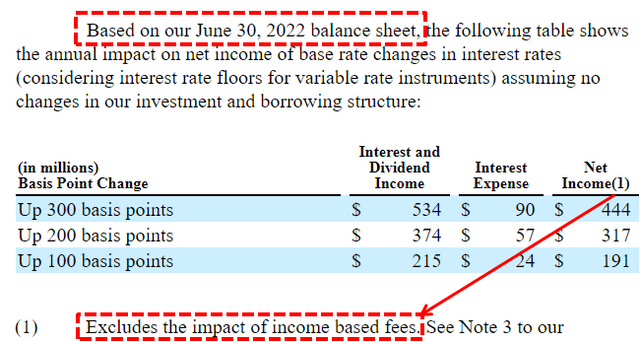

ARCC discloses a basic amount of information and is a good example of what you will find, including the following table provided each quarter. The footnote at the bottom is important and most BDCs do not include the potential incentive fees paid (or reduced) when disclosing impacts to net investment income (“NII”). This is because these amounts depend on many factors, including hurdles. In the following analysis, I have included these fees for each BDC when calculating the potential impact on NII.

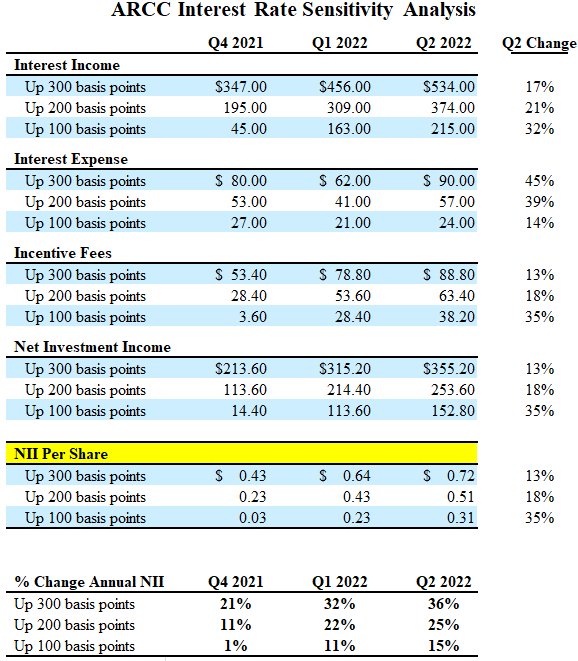

The following table shows the change from Q4 2021 to Q2 2022 with the impact from a 100 basis points increase changing from an additional $0.03 per share of annual earnings (as of December 31, 2021) to $0.31 per share (as of June 30, 2022).

ARCC Call: “We don't believe a tightening monetary cycle will have negative effects on us. Our large weight floating rate loan portfolio is financed by mostly fixed rate unsecured sources of financing and our assets are largely floating rate investments. We believe this positions us well to have our net interest earnings benefit from rising rates.”

Almost every BDC carefully matches assets and liabilities, including floating or fixed, term, and risk. The following items are some items to keep in mind:

Fixed-rate borrowings typically are at higher rates than variable-rate credit facilities

Credit facilities have unused line fees

Most floating-rate investments have floors 25 to 100 basis points (reached earlier this year for most investments)

Some portfolio companies will prepay loans

Prepayments often drive fee income

Capital from prepayments is typically used to repay variable-rate credit facilities

New investments for most BDCs have been at higher yields

Incentive fees need to be considered for both positive and negative impacts

The following tables show the side-by-side Interest Rate Sensitivity Analysis for each BDC along with rankings and projections of which are the most likely to increase dividends.