HTGC Quick Update: Free Version

The following information was previously provided to paid subscribers of BDC Buzz along with:

HTGC target prices/buying points

HTGC risk profile, potential credit issues, and overall rankings

HTGC dividend coverage projections (base, best, worst-case scenarios)

Real-time changes to my personal portfolio

For paid subscribers, please access the full HTGC Deep Dive Projection report at the following link:

HTGC Dividend Coverage Update

Hercules Capital (HTGC) reported between its best and base case projections for Q2 2021 due to higher-than-expected fee income (discussed below) fully covering its dividend. The company has covered its dividend by an average of 109% over the last 8 quarters with around $1.38 of undistributed income to support the previously announced supplemental dividends.

“The main driver for the increase was fee income despite lower payoffs largely due to the vintage and size of the onetime and unamortized fees associated with the loans that paid off.”

The effective yield was 12.7% during Q2 2021, compared to 13.3% for Q4 2020 due to lower early loan repayments. Effective yields generally include the effects of fees and income accelerations attributed to early loan repayments and other one-time events. HTGC’s ‘Core Yield’ decreased from 11.6% to 11.5% and over 98% of its debt portfolio is now at its contractual interest rate floor.

“Our effective and core yields in the second quarter were 12.7% and 11.5% respectively compared to 13.2% and 11.6% in the first quarter. The effective yield was down due to the lower early repayments and the slight decline in the core yield was due to a modest decrease in coupon interest.”

HTGC ended Q2 2021 with $610 million of available liquidity, including $18 million in unrestricted cash and cash equivalents, and $592 million in available credit facilities. The company had pending commitments of $403 million as of July 26, 2021, but management is expecting higher amounts of prepayments between $200 million and $250 million that could drive a higher effective yield for Q3 2021 (similar to Q4 2020) and is taken into account with the updated projections.

“Early loan repayments were at the mid-range of our guidance of $150 million to $200 million at nearly $170 million, but decreased slightly from $192 million in Q1. For Q3, we expect prepayments to be between $200 million and $250 million based on the momentum that we are seeing across our investment portfolio, although this number could change materially as we progress in the quarter. In terms of what's driving, the elevated prepayments for Q3, I think a couple of things. Our portfolio right now is performing at a level that we frankly haven't seen in some time and the lot of these companies are incredibly well capitalized. Right now we have per our disclosure eight companies in the pending IPO SPAC position and so we expect at least a good portion of those to be completed in the Q3 timeframe and then we're also aware of several M&A potential events and capital raising events in Q3, which we expect to lead to elevated prepayment. So it's all being driven by positive things and I think the credit, as I said in my comments really goes to our team, who is doing an incredible job, picking and selecting and winning mandates and financing opportunities with just some great companies that are incredibly healthy and have a lot of optionality.”

Since the close of Q2 2021, the company has closed new debt and equity commitments of $27 million and funded $23 million. Also taken into account with the updated projections is the following guidance from management including operating expenses of $16.5 million to $17.5 million and increased borrowing costs from the early redemption of its Baby Bond “HCXZ” as discussed in the previous report and below:

“Our core yield guidance of 11% to 12% continues to apply for Q3 2021. For the third quarter we expect SG&A expenses of $16.5 million to $17.5 million consistent with the prior quarter. Although we expect our underlying third quarter cost of borrowing to decreased modestly, interest and fees will increase with the accelerated fee recognition of $1.5 million due to the previously disclosed early redemption of $75 million of 5.25%, 2025 notes completed on July 1 at par value. The $1.5 million increase in fee recognition is a one-time event and will impact our Q3 NII. In addition, we expect our two securitizations, which are now in natural run-off to continue to trigger an increased capitalized fee recognition. With respect to the February 2022 convertible bond maturity, we expect to settle any converting holders with cash for the principal component of the note and shares for the option value. This will allow us to pay the principal in cash irrespective of the number of conversions while managing leverage and dilution appropriately.”

In October 2020, the company announced that it had received approval for its third SBA license providing an additional $175 million of fixed-rate borrowings at very attractive 10-year rates.

“We continue to utilize our third SBA license drawing down an additional $16.2 million of debentures and an attractive annual interest cost of 0.71%. We had access to an additional $121.3 million of SBA funding for qualified investments.”

During Q2 2021, the company did not issue additional shares through its At-the-Market (“ATM”) Equity Distribution Agreement. HTGC continues to target a regulatory debt-to-equity ratio between 0.95 to 1.25 and will likely use the ATM program to maintain leverage while growing the portfolio. As of June 30, 2021, approximately 16.2 million shares remain available for issuance and sale.

“Our target ceiling that we've self-imposed on ourselves 1.25 leverage to equity and we would see as prepayments start to stabilize again that we would try to target to get back above one-to-one for sure.”

HTGC maintains a “variable distribution policy” with the objective of distributing four quarterly distributions in an amount that approximates 90% to 100% of the company’s taxable quarterly income or potential annual income. In addition, the company pays additional supplemental distributions to distribute approximately all its annual taxable income in the year it was earned, or it can elect to maintain the option to spill over the excess taxable income into the coming year for future distribution payments.

“We have a variable dividend policy, so it's something that the Board evaluates on a quarterly basis, and we don't just look short-term, we look long-term when we're making those decisions. We've been very clear in terms of our public guidance on the last several calls that we see absolutely no risk to that $0.32 base distribution, and we would reiterate that guidance on this call now. If you think about what we've been able to do in terms of the special distributions, we've been able to deliver to our shareholders a supplemental or a special distribution in six of the last seven quarters on top of the $0.32 base distribution. And obviously, subject to market conditions, I think one of the things that we're going to look at near-term here is trying to find a way to provide a little bit more consistency and continuity to those supplemental distributions. “

As predicted in the previous report, HTGC announced that its Board has declared additional supplemental cash distributions during 2021 due to the “record level of spillover” and “the trajectory of the business for the course of 2021”. HTGC will be distributing $0.28 per share evenly over the next four quarters starting with $0.07 per share starting with Q2 2021

“As of Q2 2021, we have generated record undistributed earnings spillover of approximately $160.2 million or $1.38 per share subject to final tax filings. This provides us with additional flexibility with respect to our variable base distribution going forward and the ability to continue to invest in our team and platform. Year-to-date, we have continue to add talent to our team with several new hires. We have also continued to enhance our infrastructure and platform.”

On the recent earnings call, management was asked about the dividend policy as it relates to the tax requirements of a being registered investment company (“RIC”). My takeaway is that the $0.28 per share paid over four quarters was required for the previous amounts of undistributed/spillover income and the company will announce additional amounts to be paid out in October 2021:

Q. “So you have a record $160 million or $1.38 per share there, so can you talk bit about what your plans are with that and can you remind me if you have any restrictions there with how much spillover you can have is that 90% of NII or net assets. And then when would you need to do something if there are restrictions?”

A. “Our quarterly base distribution is variable, the board evaluates on a quarterly basis will be what we think makes sense based on the facts and circumstances as of the time. And then at the beginning of this year in Q1, we announced the $0.28 supplemental distribution for 2021, which will be distributed $0.07 per quarter in each of the four quarters of 2021. Our plan would be to evaluate at the end of this year, a further potential supplemental distribution program for 2022 and we will of course on a quarterly basis reevaluate what base distribution level we think is most appropriate. As a registered investment company, we're required to distribute 90% of our earnings basically over a year. So if we accumulate on the ordinary income earnings that are greater than 90% of annual earnings, then we're reaching that ceiling that you're talking about. So we would have to distribute it. And then on the capital gain side we have to distribute about 98% of it, but that measurement period is really from November to October, and so we need to see what that position would be after October.”

HTGC remains a ‘Level 1’ dividend coverage BDC implying a stable to growing regular dividend with the potential for supplemental dividends partially due to its internally-managed cost structure and equity investments historically providing realized gains and supporting supplemental dividends:

“Our warrant and equity portfolio is designed to provide potential upside returns to our shareholders above and beyond our net investment income, as well as mitigate potential debt losses that may occur.”

HTGC Portfolio Credit Quality Update

There was another increase in HTGC’s net asset value (“NAV”) per share of 3.1% (from $11.36 to $11.71) mostly driven by mark-to-market of its equity and warrant positions:

“Our $60 million of net change in unrealized appreciation was driven entirely by the mark-to-market of our equity and warrant portfolio. Our debt portfolio was relatively stable with a $1.5 million appreciation was mainly from the reversal of prior unrealized depreciation.”

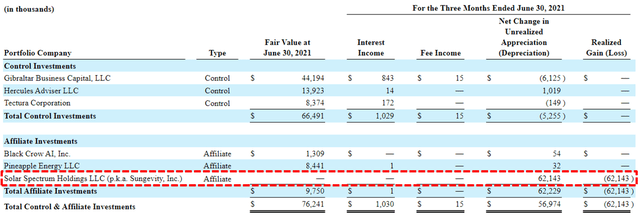

During Q2 2021, there were $14.3 million of net realized losses during the quarter due to finally exiting its legacy equity position in Solar Spectrum Holdings (Sungevity, Inc.) driving a realized loss of $62.1 million partially offset by $47.9 million in realized gains (mostly related to DoorDash and TransMedics Group).

However, there was no impact to NAV per share due to already being written off and there is possible NAV upside as discussed on the recent call:

“The net realized loss in the quarter of $14.3 million comprised of $47.86 million of net gains from the disposal of equity positions offset by $62.1 million of realized loss pertaining to one legacy equity position [Solar Spectrum Holdings LLC (p.k.a. Sungevity, Inc.)] that had previously been fully impaired at a carrying value of zero dollars. The legacy Sungevity Solar Spectrum position. That company has been on our books going back now five or six years. It was fully impaired down to a carrying value of zero several years ago when that company went through bankruptcy. We obviously continue to work on the investment. What caused us to take the realization this quarter and move it from unrealized to realized is the fact that the company has officially now been resolved. So from a GAAP perspective, we are able take that realization. It has no impact at all on that asset value. And then I would just add that, as we from a fiduciary perspective continue to look to create value from all of our positions as part of the sort of final dissolution of that company, we did structure our new deal where we were able to transfer the legacy assets, which we do believe continue to have some value into NewCo and that NewCo per our public disclosure is now right in the middle of a publicly disclosed reverse merger. So we are hopeful that on a go-forward basis, we will continue to have some possibility of realization downstream.”

HTGC still has 200,000 shares of DoorDash (DASH) that were valued at $33 million over cost as of June 30, 2021, likely driving meaningful realized gains over the coming quarters that could be used to pay additional supplemental dividends.

“We did have a record approximately $47 million of gross realized gains from distributions of our public equity and warrant positions in the quarter, the most meaningful dissolution was DoorDash we did sell a portion of that position, not the entirety of the position. As of the end of Q2, we continue to hold approximately 200,000 shares of DoorDash, which depending on which day we're using for the closing has a value of approximately $35 million to $40 million and then we had some smaller assets and sales during the quarter, but that was the most meaningful sale.”

Also, HTGC still has 1,668,337 shares of Palantir Technologies Inc. (PLTR) valued at almost $44 million which is almost $34 million above cost as of June 30, 2021.

It is also important to note that DASH and PLTR are just two positions that could deliver meaningful realized gains and NAV growth over the coming quarters especially as market prices continue higher. Please see the end of this report for additional details.

HTGC held equity positions in 67 portfolio companies with a fair value of $229.9 million and a cost basis of $133.8 million as of June 30, 2021. On a fair value basis, 62.6% or $143.9 million is related to existing public equity positions.

HTGC held warrant positions in 93 portfolio companies with a fair value of $46.7 million and a cost basis of $25.1 million as of June 30, 2021. On a fair value basis, 31.4% or $14.7 million is related to existing public warrant positions.

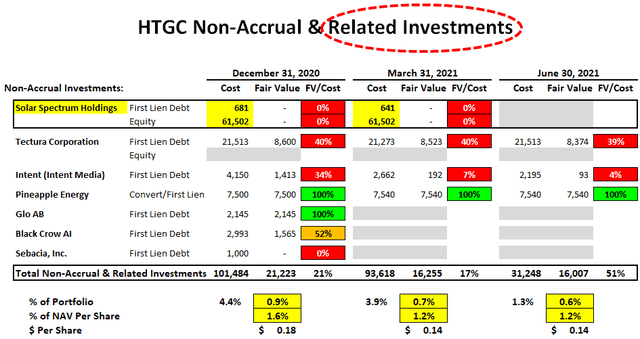

Non-accruals remain low at 0.3% of the portfolio fair value. It should be noted that the following table shows all investments that are on non-accrual status as well as other investments related to those companies.

Full HTGC Report:

Again, for paid subscribers, please access the full HTGC Deep Dive Projection report at the following link:

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means that investors need to do their due diligence before buying.