HTGC Update: Another Rock Star Quarter (All Accounts)

HTGC Update: Another Rock Star Quarter (All Accounts)

Please use the following link to access all the recently updated reports, including side-by-side comparison reports and individual company updates:

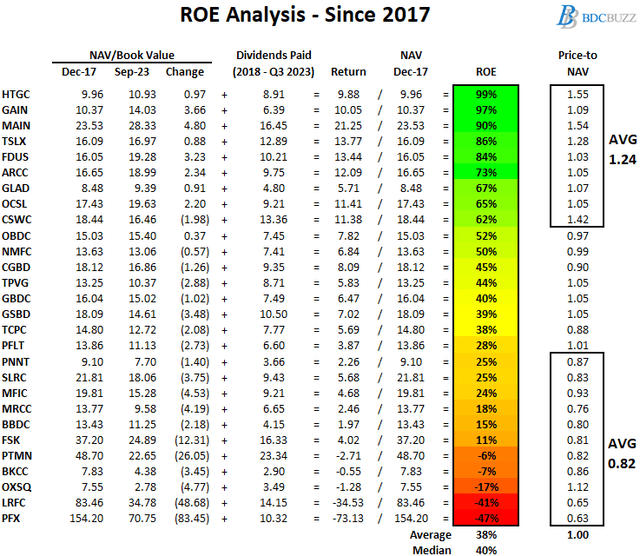

Comparison of Return on Equity (“ROE”)

This information will be updated to take into account December 31, 2023, results.

The following table shows the changes in NAV per share and dividends paid between December 31, 2017, and September 30, 2023, as a simple proxy for return on equity (“ROE”) to shareholders. It is important to note that many BDCs prefer not to pay special or supplemental dividends unless necessary because they directly reduce NAV per share. Also, some BDCs purposely pay lower dividends relative to their earnings, which contribute to higher NAV per share. However, this table takes these into account along with the current price-to-NAV ratios, showing that investors pay higher multiples for BDCs that deliver higher returns to shareholders.

Most BDCs with higher ROEs have historically held higher amounts of equity investments, especially HTGC 0.00%↑ , GAIN, MAIN, FDUS, ARCC, GLAD, and CSWC. However, TSLX has relatively lower amount amounts of equity positions and much higher first-lien currently around 91% but has still delivered higher returns to investors as shown below.

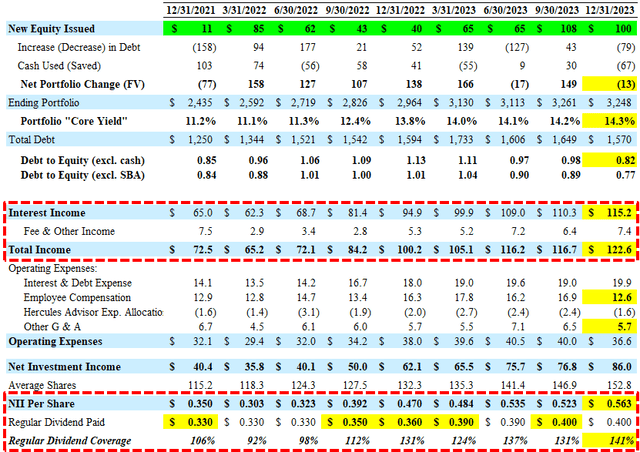

HTGC 0.00%↑ Quick Quarterly Update (December 31, 2023)

Earnings: Beat its best-case projected NII covering its regular dividend by 141% mostly due to higher prepayment-related income from $278 million of early loan repayments (compared to $148 million the previous quarter) combined with lower expenses including employee compensation and ‘Other G & A’. Also, there was another quarter of higher-than-expected fee income of over $7 million and increased portfolio yield. HTGC has undistributed earnings of $0.80 per share (previously $1.03 per share) for additional supplemental dividends.

Subsequent Events: Q1 2024 is off to a strong start as the company has closed new gross debt and equity commitments of $552 million and funded $384 million through February 13, 2024, with pending commitments of $507 million.

Dividends: Maintained its regular/base dividend of $0.40 per share plus another supplemental of $0.08 per share which was the previous base case projections. The company expects to pay a total of $0.32 per share in supplemental dividends for 2024 which was already taken into account with its ST target price and included in the total yield in the BDC Google Sheets

Recent Share Issuances: During Q4 2023, the company sold 6.5 million shares under its equity ATM program for net proceeds of $100 million. As of December 31, 2023, approximately 17.3 million shares remain available for issuance and sale.

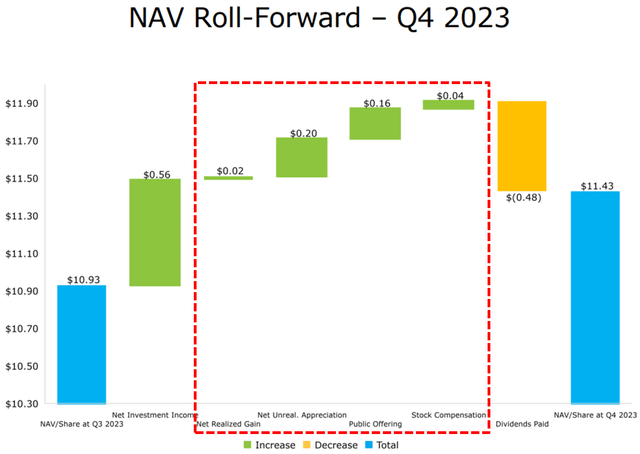

NAV Per Share: Increased by $0.50 or 4.6% (from $10.93 to $11.43) due to $0.08 per share related to the valuation on publicly traded equity/warrant positions, accretive share issuances adding $0.16 per share, overearning its regular and supplemental dividends by $0.08 per share, and appreciation of other equity and watch list positions.

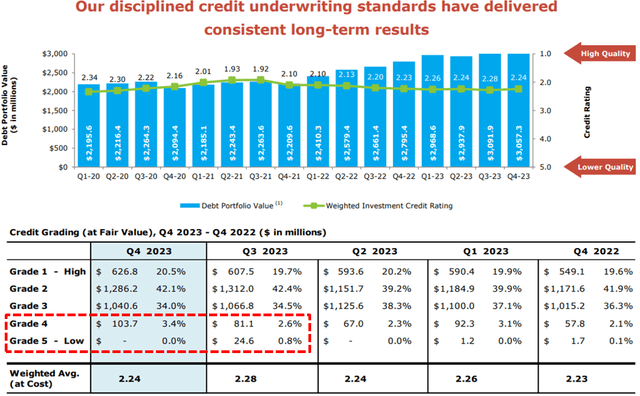

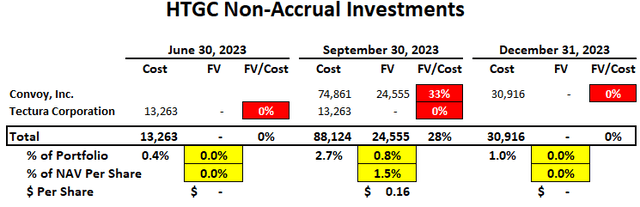

Credit Quality: Non-accruals declined from 0.8% to 0.0% of the portfolio fair value due to partial repayment of its first-lien position in Convoy, Inc. which remains the only investment on non-accrual but management is expecting to resolve the issue with no further impact to NAV per share (see notes below). The non-accrual PIK portion of its debt position in Tectura Corporation was restructured into a preferred equity position and the non-PIK loan was marked to full value. There was a decrease in the average credit grade of debt investments (from 2.28 to 2.24) and credit quality remains strong with “100% of our debt portfolio companies remain current on contractual payments”.

This information will be discussed in the updated HTGC Deep Dive Projection report.

“As of our most recent reporting, 100% of our debt portfolio companies remain current on contractual payments to Hercules. Our workout efforts with regards to Convoy remain ongoing and our recovery efforts will likely wrap up early this year, although that situation remains ongoing and fluid.”

“Early loan repayments increased in Q4 to approximately $278 million, which came in above our guidance of $150 million to $250 million. We expect 2024 to be another year with higher-than-normal volatility and a higher-for-longer rate environment, but as we discussed on our last call, we expect the market environment for new originations to improve throughout 2024. We are already seeing this come to fruition in Q1.”

Q. “It's clearly a record quarter of results, and as you noted, dividend coverage on a core basis totaled 140%. So, it would seem like the starting point for earnings in 2024 is quite a bit higher than the base dividend you announced yesterday. So, could you just walk us through the rationale about maintaining and not increasing the current base dividend?”

A. “I think we've been pretty consistent over the course of the last several years in terms of how we manage the base distribution. We never want to set the base distribution at a number that we think would jeopardize our ability to maintain it irrespective of market and rate environment conditions. We set the base distribution based on our outlook for core income, where we essentially back out the benefit of any prepayments and accelerations. We want to continue to take a conservative position. That was the choice that we made with respect to Q4. We are continuing to deliver that out-performance to our shareholders via the supplemental distributions. This is the fourth consecutive year where we've been able to enhance the quarterly base distribution with an additional supplemental distribution. And we think that that's the right way to operate the business in the current environment. It certainly does not mean that that's not going to change on a go-forward basis. But that was the rationale for the decision to maintain $0.40 and declare a $0.32 supplemental distribution payable $0.08 per quarter in 2024.”

“Hercules was able to deliver another year of record financial performance, maintain strong credit quality and achieve year-over-year portfolio growth against a challenging market environment. We capped off 2023 with record total investment income and net investment income for the fourth quarter, up over 22% and 38% year-over-year, respectively. In addition, we delivered record gross fundings of $1.6 billion for the year, an increase of over 9% year-over-year. For the full year, we achieved record total investment income and record net investment income, each growing over 43% and 62% year-over-year, respectively. We are very pleased to note that our Hercules Adviser funds delivered its first distribution, which is to the direct benefit of HTGC shareholders.As we enter our 20th year of investment activity, we remain competitively very well positioned to continue growing our platform and delivering best-in-class shareholder returns. Given the scale that we have achieved with the Hercules platform combined with our historically strong credit performance, we are maintaining our current base cash distribution and declaring a new supplemental cash distribution program for 2024.”

“Our Grade 1 and 2 credits improved to 62.6% compared to 62.1% in Q3. Grade 3 credits were slightly lower at 34% in Q3 versus 34.5% in Q3. Our rated four credits increased moderately to 3.4% from 2.6% in Q3, and we had no rated five credits in Q4. In Q4, the number of loans on nonaccrual decreased by one.”