NEWT Update: Q2 2021 & Discussion Of 2022

Summary

Plenty covered in this update including NEWT’s recently reported results with ANII of $1.197 per share mostly due to higher origination fees associated with its PPP loans.

NAV per share increased by 0.6% but $8 million of depreciation from controlled investments. No updated 10-Q so we do not have the details including non-accrual information.

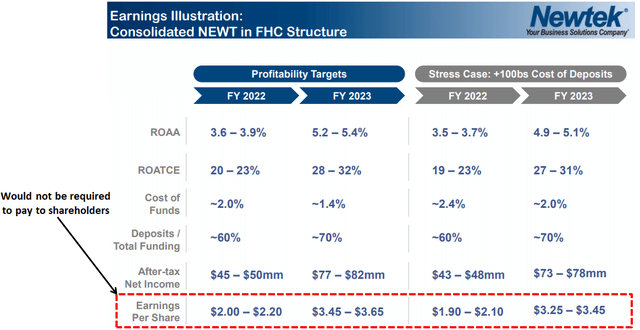

My primary concern is the $amount of expected dividends in 2022. Management just released a 2nd addendum to its previous presentation still projecting 2022 earnings of $1.90 to $2.20.

However, nothing has been provided regarding dividend policy and continuing to pay 90%-100% (previous policy). Please see the quick pricing/yield discussion below and will be included in a public article.

Most subscribers are/were attracted to the growing NAV per share and higher amounts of dividends that were required to be paid as RIC/BDC. I would suggest voting "no" on withdrawing its election to be treated as a BDC.

Other Recent Subscriber Updates:

This update discusses Newtek Business Services (NEWT) which currently is an internally-managed BDC with a differentiated and diversified business model providing multiple streams of revenue including loan origination, including SBA 7a loans, 504 loans, PPP loans (Paycheck Protection Program), and conventional loans. Also, the company provides various services to small and medium businesses including electronic payment processing, payroll processing, web solutions, insurance services, and technology.

Most of this information will be included in an upcoming public article which could have an impact on pricing as this is a volatile stock.

On August 2, 2021, NEWT announced the purchase of a small bank National Bank of New York City (“NBNYC”) and it will be asking shareholders to vote on withdrawing its election to be treated as a business development company. This means that the company would no longer have Regulated Investment Company (“RIC”) status in favor of being a financial holding company ("FHC"). As a RIC, NEWT was required to pay 90% of taxable income but if it converts to an FHC, NEWT will not be required to distribute 90% taxable income annually.

It should be noted that this was not discussed directly in the August 10, 2021, earnings announcement and press release but did include the following commentary:

Commenting on the Company’s recent announcement to acquire NBNYC, Mr. Sloane said, “We believe this planned acquisition will give us an enhanced opportunity to provide the Newtek-branded financial and business solutions to the over 30 million small- to medium-sized businesses in the U.S., as defined by the Small Business Administration. The Company believes that the acquisition of NBNYC will be accretive to long-term shareholder value and presents an enhanced structure for our growth-oriented business model. We believe our conversion to a bank holding company can potentially broaden our investor base to include more institutional stock ownership, investors that invest in index funds comprised of companies included in indices such as the Russell and S&P, and investors that have been discouraged from investing in BDCs due to the acquired fund fees and expenses (AFFE) rule.”

The portion that stands out for me is "accretive to long-term shareholder value" as compared to the shorter-term impact to shareholders. As mentioned in the Monday morning weekly update:

My personal opinion is that management did not adequately prepare its investors for such a change, likely started this process a long time ago and this will have an impact on ‘trust in management’ which is critical when investing in BDCs.

The company declared a Q3 2021 cash dividend of $0.90 per share payable on September 30, 2021, to shareholders of record as of September 20, 2021. NEWT’s current 2021 annual dividend forecast indicates a remaining dividend payment of $1.05 per share for Q4 2021, at the midpoint of the 2021 annual dividend forecast range of $3.00 per share to $3.30 per share.

Quick Discussion of 2022

As mentioned in each previous NEWT update, my primary concern is the amount of expected dividends in 2022 which is what I use for target prices. The following is commentary from the recent earnings release:

While it’s clear that some of our quarterly year-over-year comparisons have been affected by the uneven distribution of PPP income over the first and second quarters in 2020 and 2021, which income is not expected to be recurring, we are very excited to move forward and redeploy our resources back to our and our portfolio companies' lending product mix of SBA 7(A) loans, SBA 504 loans, non-conventional conforming loans, and secured lines of credit, during the second half of the year and beyond. We want to clearly convey to the market that we anticipate Newtek and its portfolio companies lending products to be at the forefront of our growth, replacing the pandemic-oriented PPP loan program."

"We note that income earned in connection with the PPP for the six months ended June 30, 2021, should not be viewed as recurring. Resources used to generate PPP loans are being focused on other more traditional activities. SBA 7(A) originations produce interest income, servicing income, and capital gains income, which is treated differently, from an accounting standpoint, than income derived from the origination of PPP loans. Both the income from originating PPP loans and SBA 7(A) loans are considered qualified forms of income for a BDC."

As mentioned earlier this week, NEWT’s management is working to repair trust (due to the ~30% decline in stock price) and the company has now released two addendums to its "August 3, 2021, Presentation".

The following disclosure was provided in the presentation:

In addition to factors previously disclosed in our reports filed with the SEC and those identified elsewhere in this Presentation, the following factors, among others, could cause actual results to differ materially from forward-looking statements or historical performance: our ability to obtain regulatory approvals (and the timing of such approvals) and meet other closing conditions to the Acquisition; modification or termination of certain businesses to comply with regulatory requirements; the risk that any announcements relating to the proposed Acquisition could have adverse effects on the market price of our common stock; difficulties and delays in integrating the NBNYC business; diversion of management’s attention from ongoing business operations and opportunities; our ability to operate as a bank holding company and the increase in regulatory burden and compliance costs; the attractiveness of our banking products to our existing customer base and our ability to cross-sell; any change in our dividend payout due to no longer operating as a BDC and RIC.

The following slides are from the most recent addendum on August 10, 2021, showing projected earnings of $1.90 to $2.20 for 2022. Again, the company would not be required to pay 90% to shareholders but helps to provide estimates for shareholders including peer group price-to-earnings ratios between 10 to 18 implying a stock price of $18.24 (using lower end 2022 earnings and bank multiples) to $39.60 (using higher end 2022 earnings and fintech multiples).

NEWT's previous LT target was $26.50 but that was based on paying a certain amount of dividends over the longer term. Using the average expected earnings of $2.05 and assuming that the company paid out 100% to shareholders (not likely) would be an implied yield of 7.7% which is below the average BDC currently at 8.5%. I will leave NEWT in the Google Sheets for now but this is now a "trading position" so please expect upcoming pricing volatility. Also, I will continue to cover in the hopes that it remains a BDC.

Again, most subscribers are/were attracted to the growing NAV per share and higher amounts of dividends that were required to be paid as RIC/BDC. I would suggest voting "no" on withdrawing its election to be treated as a BDC.

NEWT Q2 2021 Results

NEWT uses Adjusted Net Investment Income (“ANII”) as a measure of its operating performance which includes short-term capital gains from the sale of the guaranteed portions of SBA 7a loans and a non-conforming conventional loan, capital gain distributions from controlled portfolio companies, which are reoccurring events. Additionally, NEWT’s business model is seasonal/cyclical in nature which is why the company pays an irregular/variable quarterly dividend and is managed on annual basis (not quarterly).

For Q2 2021, NEWT reported ANII of $1.197 per share mostly due to higher origination fees associated with its Payment Protection Program (“PPP”) loans:

NEWT’s NAV per share increased by 0.6% but the company has not released its updated 10-Q so we do not have the details as well as non-accrual information. However, there was $7.9 million of unrealized depreciation from its controlled investments with no associated/offsetting dividend income.

The last three lines in the table below use the average over the last four quarters to help identify trends in dividend coverage.