Preview: GSBD Potential July Pullback

The following information was previously provided to subscribers of BDC Buzz along with:

GSBD target prices/buying points

GSBD expected supplemental dividends

GSBD risk profile, potential credit issues, and overall rankings

GSBD dividend coverage projections and worst-case scenarios

Real-time changes to my personal portfolio

Full GSBD Report:

Summary

GSBD has a higher-than-average yield at 9.4% (including one more special dividend of $0.05).

There is a good chance that I will be purchasing additional shares in July 2021 after the final pre-IPO share lock-up expires and will send reminders to subscribers the week before.

GSBD is for risk-averse investors with 82% true first-lien, 0.3% non-accruals, shareholder-friendly fee structure, and a higher quality credit platform.

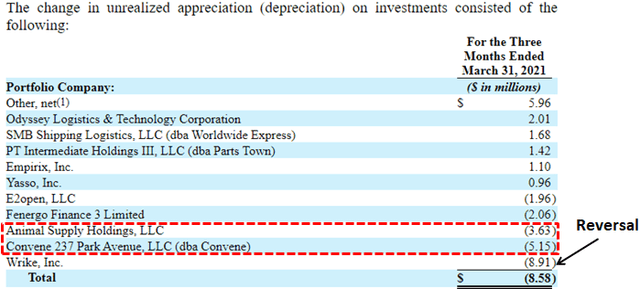

During Q1 2021, there was around $0.07 per share in realized gains.

Only one portfolio company has been added to non-accrual over the last five quarters.

Two investments that need to be watched have been discussed in previous reports (Animal Supply and Convene) which were marked down in Q1 2021 and discussed below.

Goldman Sachs BDC (GSBD)

It should be noted that there will likely be additional selling again during the first and second week of July 2021 potentially driving the stock price closer to its ST target of $18.50 and I will send out reminders before the last lock-up expires.

“….upon the closing of the Merger that generally restricted all stockholders who received shares of our common stock in the Merger from transferring their respective shares of our common stock for at least 90 days following the date of the closing of the Merger (the “Closing Date”), subject to a modified lock-up schedule thereafter (lock-up restrictions on 1/3 of the Affected Stockholders’ shares will lapse after 90 days from the Closing Date, lock-up restrictions on an additional 1/3 of the Affected Stockholders’ shares will lapse after 180 days from the Closing Date, and lock-up restrictions on the remaining 1/3 of the Affected Stockholders’ shares will lapse after 270 days from the Closing Date).

During Q1 2021, there was around $7.5 million or $0.07 per share in realized gains related to the sale of its equity investment in Wrike, Inc in March 2021:

“One notable repayment resulted in the monetization of a loan that we made originally in December 2018 and included in equity co-investment into a company called Wrike, a SaaS-based project management and cloud collaboration company, which was acquired by a strategic in March of this year. The first lien loan repayment resulted in a 10.4% IRR and was augmented by a 3.3x money multiple on the equity co-investment.”

There were no additional investments added to non-accrual which remain around 0.3% of the portfolio fair value. Only one portfolio company has been added to non-accrual over the last five quarters.

There were two investments with meaningful markdowns during Q1 2021 including previously discussed Animal SupplyHoldings and Convene 237 Park Avenue. During Q3 2020, its first-lien debt investment, preferred and common equity in Animal Supplywere exchanged for second lien debt, common equity and a right to purchase additional first-lien debt, second lien debt, and common equity, which resulted in a realized loss of $36 million or $0.89 per share. Convene focuses on shared meeting spaces directly impacted by the pandemic but has recently received additional capital from its equity shareholders and junior capital (below GSBD’s first-lien position) and “the vaccine rollouts that are really starting to take hold”:

Q. “It looks like Convene 237 Park Avenue, kind of stood out for $5 million markdown this quarter. Looks like some kind of combination of co-working or meeting space in New York City. So I appreciate this is a single name, private company. Maybe you could just give us -- maybe a little more about that business, maybe why it's getting a mark here, given that it feels like we're seemingly, hopefully, coming out of pandemic?”

A. “Yes, that's right. One of the few businesses in the portfolio, I would say, is squarely in the crosshairs of a lot of the behavioral issues associated with pandemic. So Convene is focused on providing shared meeting space services and leading -- it's a first lien investment in top of the capital structure, very well structured, leading into the pandemic, really performing quite, quite well, broadly benefiting from a trend around people wanting to optimize their real estate footprints. One of the least efficient uses of your real estate is a big shared meeting space that gets used on a less frequent basis, so big secular tailwinds driving their business. But of course, in the lockdown environments, a lot of challenges within that business, really, a remarkable, I would say, management effort to get the business's cost structure down significantly to reduce the rent payments quite significantly as well. In addition, we've had significant support from the equity shareholder base that has infused additional liquidity into the company. So we, like you, are looking forward to a bit more of a normalization of behavior more broadly. And I think in the current environment, appropriate to mark that investment down. But like I noted, we do take comfort in junior capital beneath us coming into the business and more broadly, the vaccine rollouts that are really starting to take hold here, resulting in a very different return to office, for example. And I think just more significant social interaction.”

What Can I Expect Each Week From BDC Buzz?

Weekly BDC Sector Update - Before the markets open Monday morning we provide quick updates for the sector including significant events for each of the companies that we follow along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, what to look for in the coming week, and any other meaningful economic events that need to be considered for the sector.

Deep Dive Projection Reports - Detailed reports on 2 to 3 BDCs per week prioritized by first focusing on potential issues such as dividend coverage and/or portfolio credit quality changes. We look for portfolio updates that might be mentioned in the SEC filings as compared to company announcements. Then, reports are prioritized based on pricing opportunities including equity offerings.

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.