Preview: "Parking Idle Cash At 5% To 6% Yields"

Public Article Preview:

The following update is a preview of an upcoming public article "Parking Idle Cash At 5% To 6% Yields" that will be posted on Seeking Alpha next week. Most of the information was provided (along with much more detail) in the following update from yesterday:

Other Recent Subscriber Updates:

Continued Rally in Stock Prices

The general markets have continued to rally since the March/April 2020 lows including Business Development Companies ("BDCs") which have been outperforming other higher-yield sectors especially compared to Real Estate Investment Trusts ("REITs") as discussed recently in:

2020/2021 Comparisons: "This High-Yield Sector Continues To Pummel REITs"

Longer-Term Comparisons: "REITs Continue To Underperform BDCs"

Many readers have been building cash from collecting dividends as they were actively investing in BDCs last year when they were yielding 18% as discussed:

Many stocks are near new highs and investors are asking where they should put idle cash while waiting for better entry points on common stocks.

Investing Your Temporary 'Idle Cash'

For purposes of this article, 'idle cash' is referring to capital that is not working/employed for your especially after taking into account potential inflation. Also, this article focuses on 'temporary' idle cash which is around 6 months or less so we will not be focused on 'default risk' which will be covered in the following articles for longer-term investors.

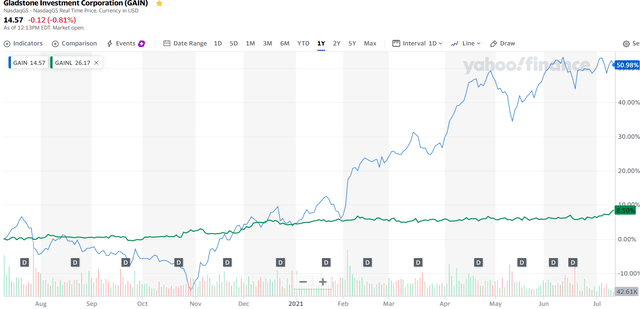

Baby Bonds (also known as exchange-traded debt) are typically for investors that would like to limit the amount of pricing volatility and overall risk in exchange for lower yields. The following charts show the price volatility for HTGC and GAIN relative to their Baby Bonds:

Source: Yahoo Finance

Redemption/Call Risk

Currently, one of the primary risks for investors investing in BDC Baby Bonds is the “redemption risk” or “call risk” especially if you pay too much on your initial purchase and hold for a short period.

Many BDCs have been working to reduce their borrowing costs through refinancing higher rate notes. It is important to take into account which baby bonds are currently "callable" and the potential for capital losses during the worst-case scenario.

Call risk is the risk that a bond issuer will redeem a callable bond prior to maturity. This means that the bondholder will receive payment of the par value of $25.00 of the bond plus accrued interest. If a bond is redeemed early, the investor will not be able to obtain the expected return or will have to re-invest the proceeds and yields on other bonds in the market. Given this, callable bonds generally pay higher interest than non-callable bonds.

The following table is from the "Baby Bonds" tab in the BDC Google Sheets which includes Call Risk Capital Loss and Breakeven Days for each baby bond as discussed below. Please make sure to check the following indicators to identify early redemption/call risk

Recommendations based on "If Called". Do not purchase at prices when "Overpriced" is showing.

YTC is the yield-to-call and is negligible/negative when showing "NM".

The Call Risk Capital Loss refers to the worst-case scenario of the bond being called tomorrow and takes into account 30 days of additional interest accrued before being redeemed.

Breakeven Days refers to the number of days of interest needed to break even given the current market price.

As of the close on July 15, 2021, GAINL, FCRW, FDUSZ, NEWTL, GLADL, and FDUSG were priced at levels that could result in capital losses if redeemed early as they are or will be callable in this year.

General notes:

BDC Baby Bonds trade "dirty" which means that there is a certain amount of accrued interest in the market price. I have included the amount of accrued interest in the table below.

The 'effective yield' is based on the current price less accrued interest.

Investors should use limit orders when purchasing exchange-traded debt such as Baby Bonds.

You need to own the Baby Bond one trading day before the ex-dividend date to be eligible for the full quarter of interest.

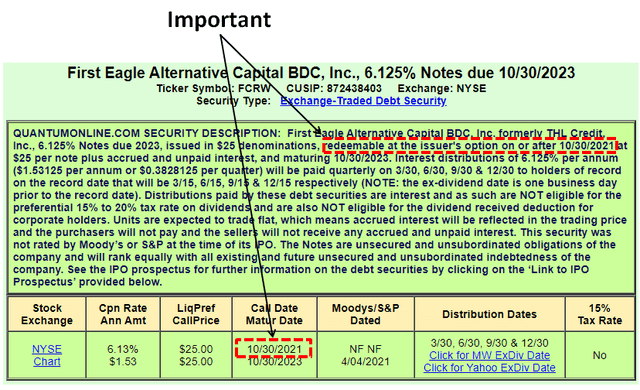

FCRW Example

As shown in the previous table, FCRW currently has a large amount of call risk due to being priced at $26.54 and callable on October 30, 2021, resulting in a potential Call Risk Capital Loss of $0.95 for each note and 331 days to break even on your investment. The following tables show how these amounts are calculated:

Source: Quantumonline

As shown in the following table, 7 baby bonds are currently callable with another 9 more later this year. Please disregard the yield-to-call ("YTC") for most of the baby bonds that are or will be callable in the near future as it is measured over 30 days and then annualized. However, it should be noted that YTC is typically used as the yield-to-worst ("YTW") for most BDC Baby Bonds.

SAF Example

Another example is SAR that just announced $125 million of unsecured notes due February 2026 partially used to fully redeem its Baby Bond "SAF" but this note is was priced appropriately just before it was announced likely assuming that it would be redeemed soon. As mentioned earlier many BDCs have been refinancing their borrowings using unsecured notes but typically at rates between 2.00% and 3.00% for most BDCs (especially through early 2026) and borrowing at a higher rate (especially over 4.00%) is likely due to portfolio credit quality similar to Apollo Investment (AINV) earlier this month. Please see the comments from 'Bekster' on the recent AINV new release:

Source: SEC Filing

Source: Yahoo Finance