TSLX Update: Solid Quarter, Supplemental Above Best-Case

TSLX Update: Solid Quarter, Supplemental Above Best-Case

Please use the following link to access all the recently updated reports, including side-by-side comparison reports and individual company updates:

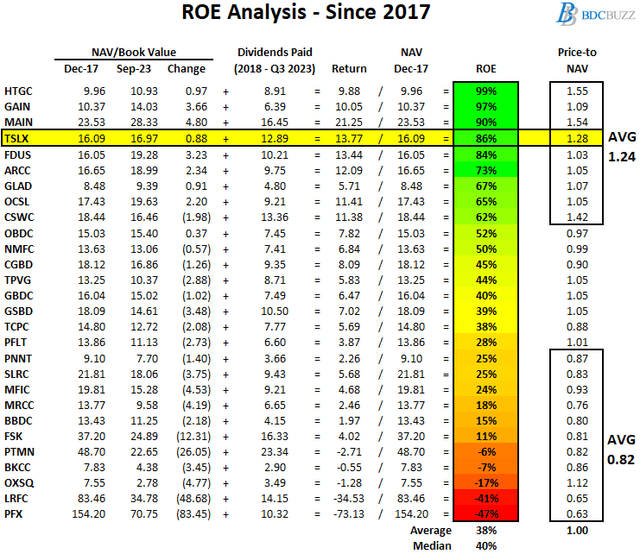

Comparison of Return on Equity (“ROE”)

This information will be updated to take into account December 31, 2023, results.

The following table shows the changes in NAV per share and dividends paid between December 31, 2017, and September 30, 2023, as a simple proxy for return on equity (“ROE”) to shareholders. It is important to note that many BDCs prefer not to pay special or supplemental dividends unless necessary because they directly reduce NAV per share. Also, some BDCs purposely pay lower dividends relative to their earnings, which contribute to higher NAV per share. However, this table takes these into account along with the current price-to-NAV ratios, showing that investors pay higher multiples for BDCs that deliver higher returns to shareholders.

Most BDCs with higher ROEs have historically held higher amounts of equity investments, especially HTGC, GAIN, MAIN, FDUS, ARCC, GLAD, and CSWC. However, TSLX 0.00%↑ has relatively lower amount amounts of equity positions and much higher first-lien currently around 91% but has still delivered higher returns to investors as shown below.

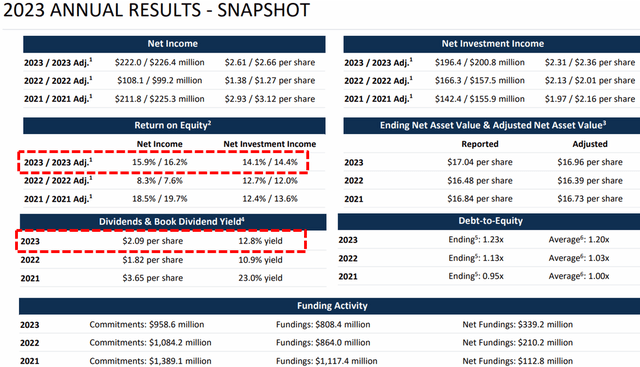

TSLX 0.00%↑ Quick Quarterly Update (December 31, 2023)

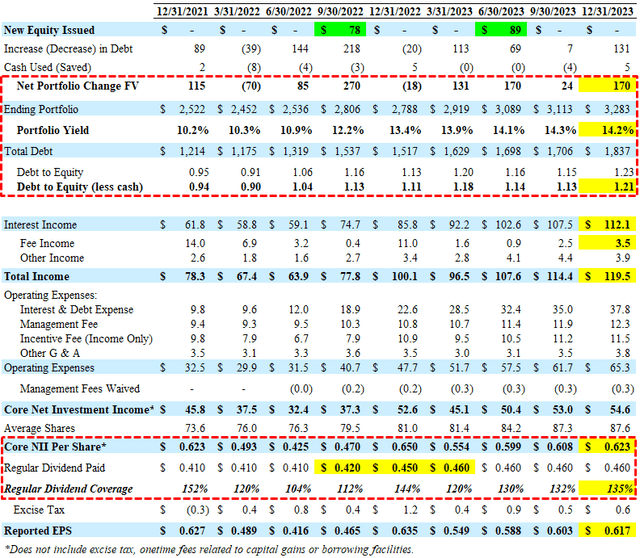

Earnings: Beat its best-case projections covering its regular dividend by 137% (excluding tax accrual) due to higher than expected portfolio growth and higher fee and prepayment-related income, including accelerated original issue discount (“OID”) accretion partially offset by a slight decline in the overall portfolio yield from 14.3% to 14.2%. Leverage increased due to portfolio growth and no shares issued through its ATM with a current debt-to-equity of 1.21 (net of cash).

Dividends: Maintained its base dividend of $0.46 plus another supplemental dividend of $0.08 for a total of $0.54 per share paid in Q1 2024, which was above the previous best-case projections of $0.53 per share.

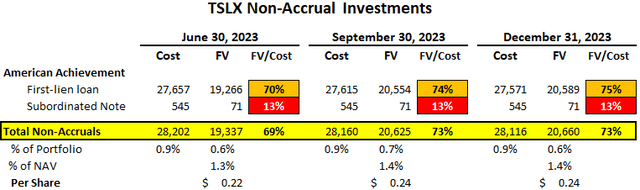

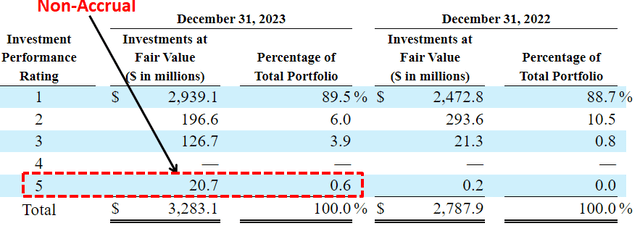

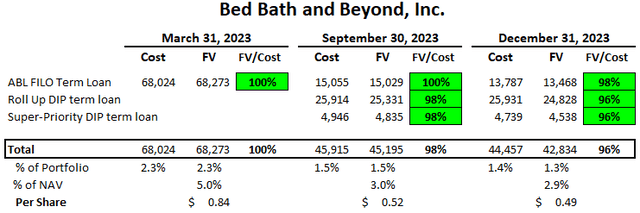

Credit Quality: Only American Achievement remains on non-accrual status at 0.6% of the portfolio fair value with almost 96% of the portfolio fair value rated 1 or 2 (strongest credit quality). It should be noted that its debt position in Bed Bath and Beyond remains almost fully valued, implying confidence from management, as discussed in the previous report. TSLX management is very skilled at finding value in the worst-case scenarios, including distressed retail ABL and energy investments.

NAV Per Share: Increased by another 0.4% (from $16.97 to $17.04) due to overearning the dividends and accretive share issuances through the DRIP.

Other: Recently issued $350 million of 6.125% unsecured notes due March 2029, as the company is continuing to strengthen its balance sheet with more unsecured borrowings.

This information will be discussed in the updated TSLX Deep Dive Projection report.